Search Knowledge Base Articles

Cryptocurrency explained

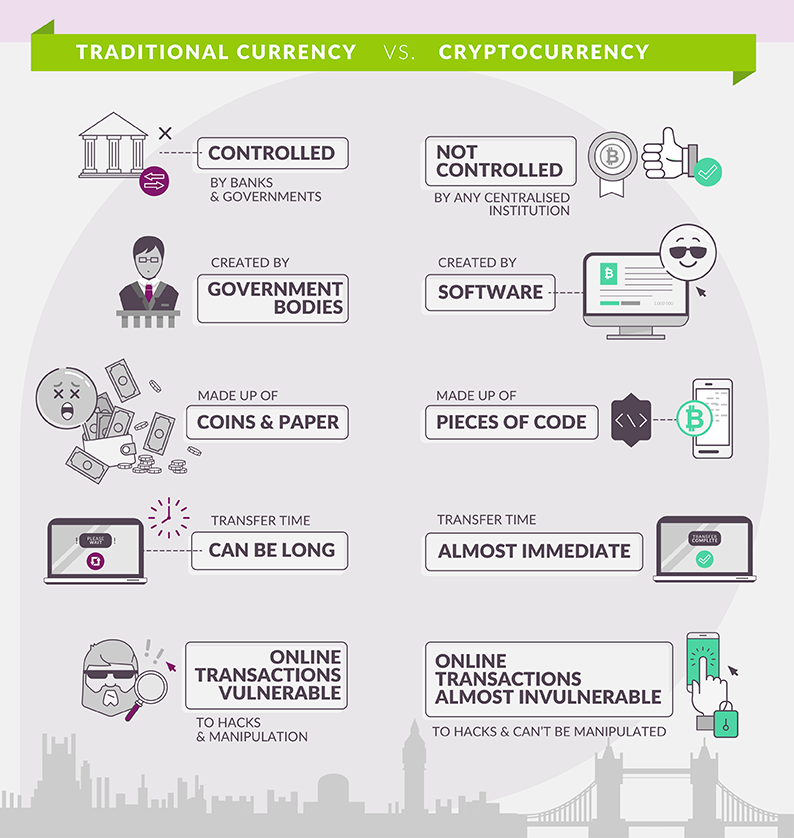

A cryptocurrency is a form of digital money. While a traditional currency is recognised by the law of the country that issues it - this is known as legal tender - a cryptocurrency is not tied to or certified by any government.

Instead, cryptocurrencies are released as open source software that anyone with an internet connection can ‘mine’. Mining is where this software offers mathematical problems that people (miners) can attempt to solve online. If they do so successfully, they are rewarded with units of cryptocurrency.

Does that mean I need to be a software nerd to get involved in cryptocurrency?

No. If you don’t feel up to mining, you can access cryptocurrency by buying it with traditional money, known as ‘fiat’, on a cryptocurrency exchange such as Coinbase, Kraken or the London Block Exchange. Blockchain technology processes the exchange transactions from person A to person B directly and securely, without having to go through a bank or government.

Furthermore, every transaction is fully transparent and securely stored. This is achieved thanks to a process called cryptography, which turns transaction information into highly secure code.

So why is cryptocurrency important?

Well, not everyone believes that it is. Cryptocurrency has its lovers and its haters.

Lots of people are interested in cryptocurrencies because:

-

They are decentralised, which means governments can’t meddle with or control them.

-

They support a high degree of anonymity, which means that you can make transactions without using your name or going through a bank. Different cryptocurrency blockchains vary in the degree of anonymity they provide – but this is something we’ll cover later.

-

They are secure. This is because of the way the transaction information is stored (on a blockchain, using cryptography).

-

There are very limited fees. As middlemen do not control or interfere with cryptocurrencies, there are minimal fees involved in making transactions.

-

They are available to everyone. You don’t need to be approved by a bank to use cryptocurrencies.

-

They are borderless. Anyone with an internet connection, anywhere in the world, can trade cryptocurrencies.

But many people are less convinced. They say:

-

As cryptocurrencies provide anonymity, they are useful for criminal transactions.

-

Their value proposition is risky, with no third party guaranteeing said value.

-

People who own digital currencies risk losing them to hacking.

-

They are volatile, which leaves investors open to potentially huge gains and losses.

What are the most common cryptocurrencies?

Bitcoin was the first cryptocurrency to hit the market in 2009 - someone, or perhaps some people, under the pseudonym Satoshi Nakamoto, invented it. They were also responsible for implementing the first Blockchain database.

Fast-forward almost a decade and there are now over 1000 cryptocurrencies available. Ethereum, Monero, Litecoin and Ripple are some examples, but the list is long and is only going to get longer!

Did you find this article useful?

Related Articles

-

Digital Currency Terminologies

ACH - ACH payments are electronic payments made from one bank to another through the Automated Clearing House network. Many people already use ACH pay...

-

Blockchain explained

Cryptocurrencies are getting a lot of attention, but there’s just as much buzz around blockchain. There’s a very good reason for this -...

-

Bitcoin explained

Bitcoin, the world’s first cryptocurrency, is something of a trailblazer. Some would argue that Bitcoin has the potential to completely change t...

-

Ethereum explained

Ethereum isn’t a cryptocurrency – it’s the name of the network that is powered by Ether (ETH), which is itself the world’s sec...

-

Litecoin explained

Litecoin is a decentralised cryptocurrency created in 2011 by ex-Google employee Charlie Lee. At this point, you could certainly be forgiven for think...